One of the questions we hear most often from prospective investors is:

“What happens if a borrower stops making payments?”

It’s a fair question.

When people first learn about peer-to-peer lending, they sometimes assume that a late loan is simply lost, or that once a loan is funded, the platform has little incentive to stay involved.

The reality is quite different.

Just like banks and other lenders, we spend a significant amount of time managing loans after they’re funded. Underwriting is only one part of lending. Servicing, collections, and recoveries are equally important.

And while nobody likes to see a loan become delinquent, late payments are a normal part of consumer lending. People lose jobs. Unexpected expenses come up. Life happens. What matters is how those situations are handled.

So, what actually happens when a borrower misses a payment?

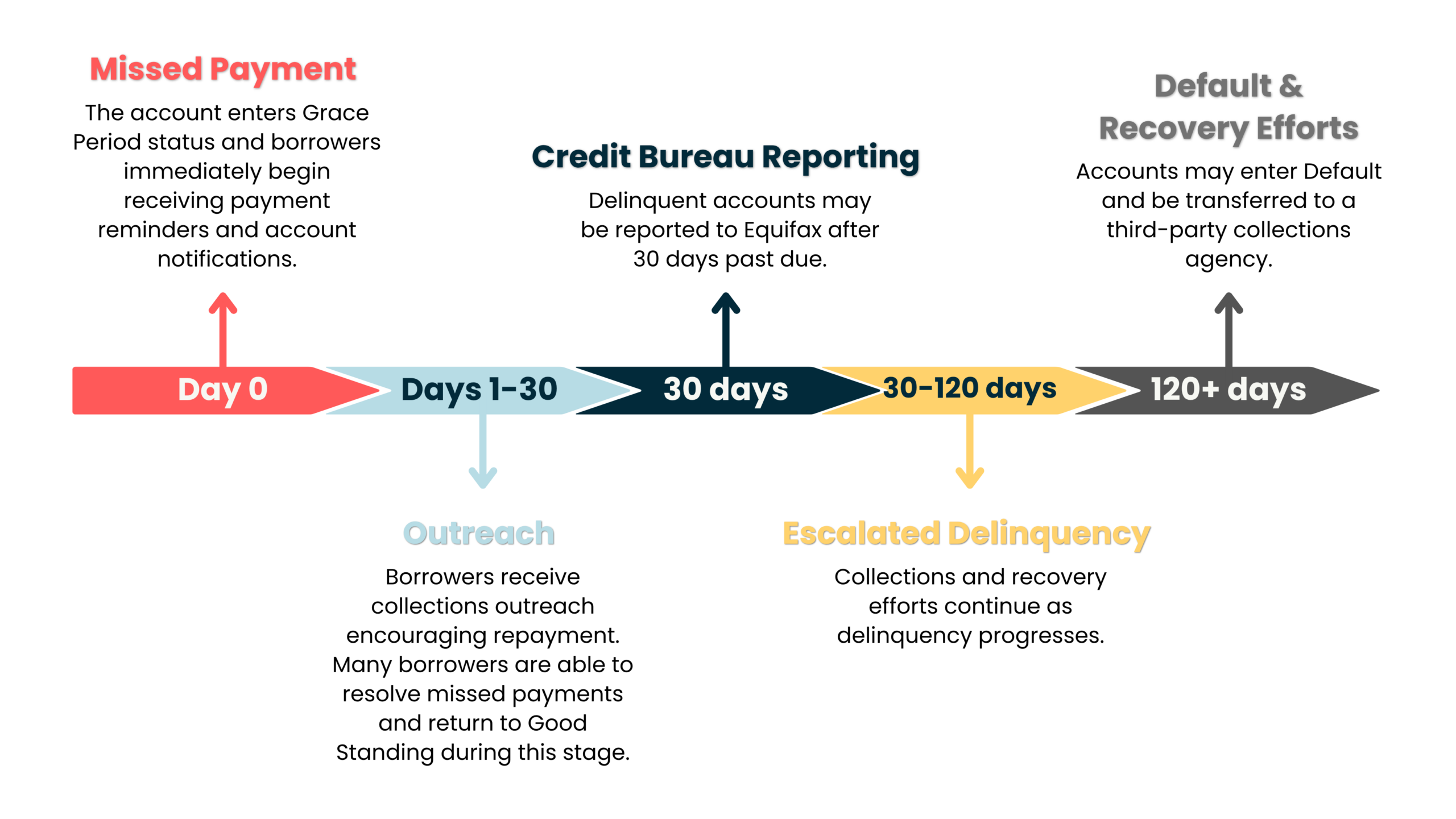

When a borrower misses a payment, the loan enters a grace period status. During this time, outreach efforts begin through automatic reminders and direct communication with the borrower.

Once the loan becomes 30 days past due, they are reported to Equifax but many borrowers are still able to recover before reaching that point. Some may catch up on payments while other may enter settlement agreements or credit counselling programs to continue repayments in some form.

goPeer Collections Process Timeline

What do loan performances actually tell us?

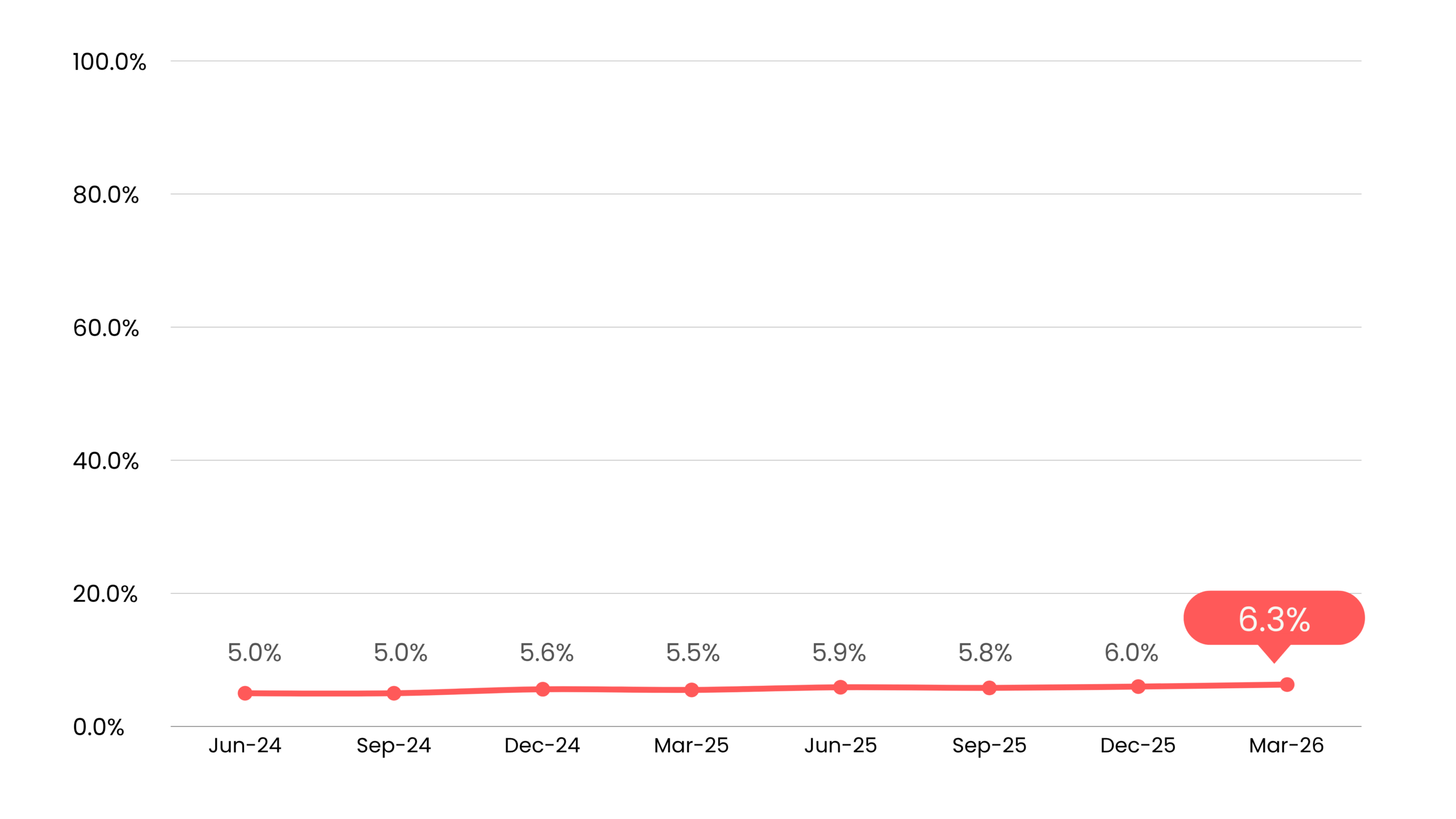

While delinquency is an important metric, charge-offs can provide a clearer picture of realized losses across the platform. Seeing these trends can help investors better understand how risk and returns can vary across the platform.

It’s also important to remember that charge-offs typically occur after extended servicing and collections efforts have already taken place.

Historical Net Charge-Off Rates

Net charge-off rates shown as of March 31, 2026. Data reflects cumulative platform performance since inception.

It’s also important to understand that delinquency does not always lead directly to charge-off.

What do recoveries look like at goPeer?

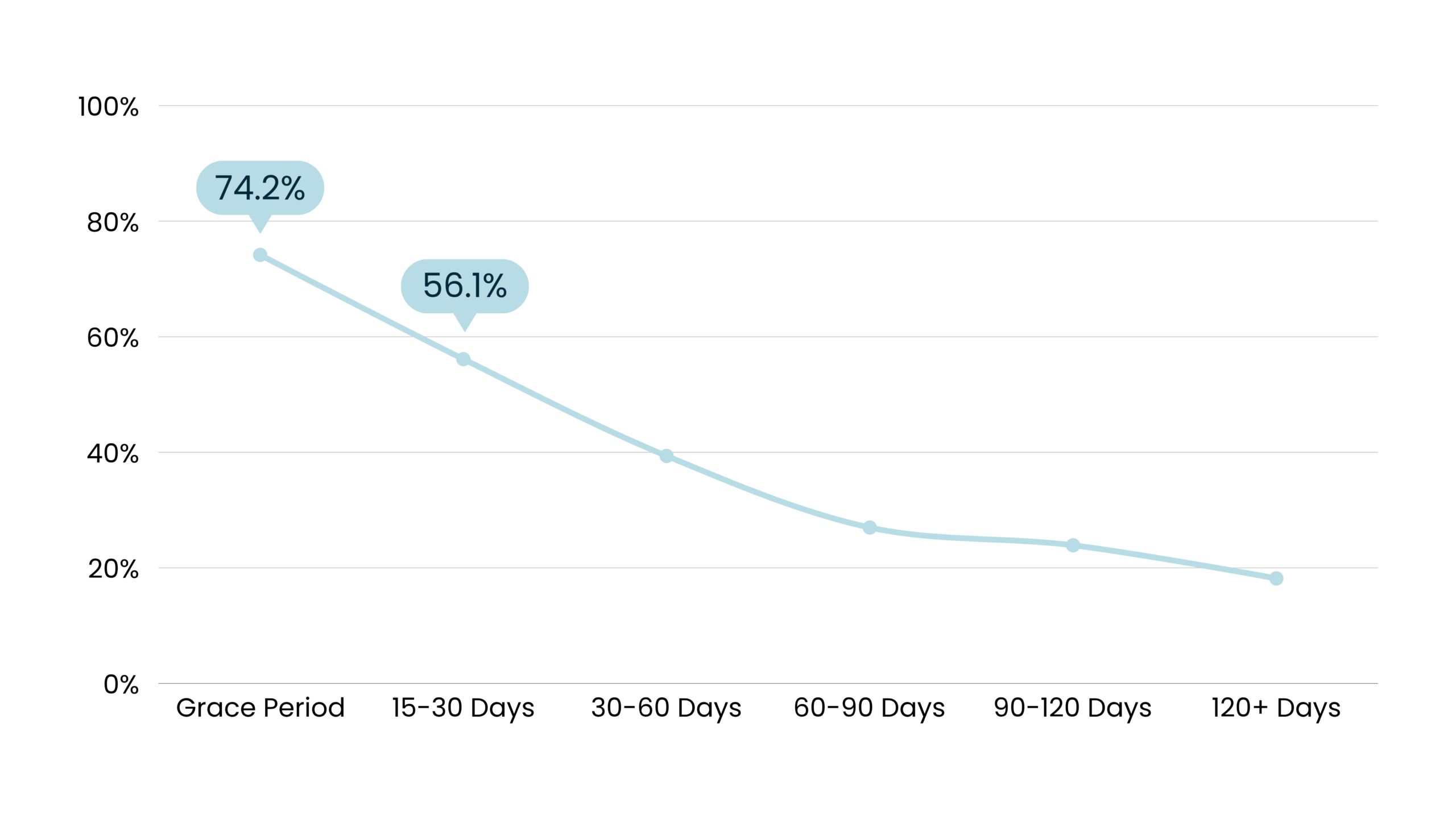

Recoveries are an integral part of the lending process. A loan becoming late does not automatically mean that that loan is permanently lost.

goPeer has a dedicated collections and servicing team focused on borrower outreach, following up repayments, and recovery efforts throughout the delinquency process. The goal is always to help borrowers return to good standing whenever possible before accounts go further into delinquency.

Based on historical internal platform data for 2024, approximately three quarters of loans entering grace period status (1-15 days late) have ultimately returned to repayment, while over half of loans that reach 15-30 days past due have ultimately resumed repayment in some form.

Recovery rates reflect the percentage of loans that returned to servicing or were paid in full after reaching each delinquency stage. Based on loans originated in 2024 and measured as of March 31, 2026.

Recoveries can happen in several ways, including borrowers catching up on missed payments, entering repayment arrangements, settling balances, or continuing repayment through credit counselling or other programs.

That’s why we don’t look at delinquency alone when evaluating portfolio performance. Some loans that become late ultimately continue repaying in some form over time.

Not all delinquency ends the same way

Some loans eventually return to current status, while others may move into settlement agreements, consumer proposals, or other repayment arrangements. Because of this, delinquency alone does not always reflect the final outcome of a loan.

Charge-offs themselves tend to have significantly lower recovery rates, which is why early servicing and collections efforts are important.

Diversification still matters

Even with a rigorous underwriting process and a comprehensive collections system in place, losses are still a natural part of lending and investing. This is why diversification is still one of the most important strategies for investors.

As investments are spread across more loans, the impact of a small percentage of delinquencies becomes smaller relative to the overall portfolio.

Historically, more diversified investor portfolios on the platform have also tended to see more consistent outcomes overall.

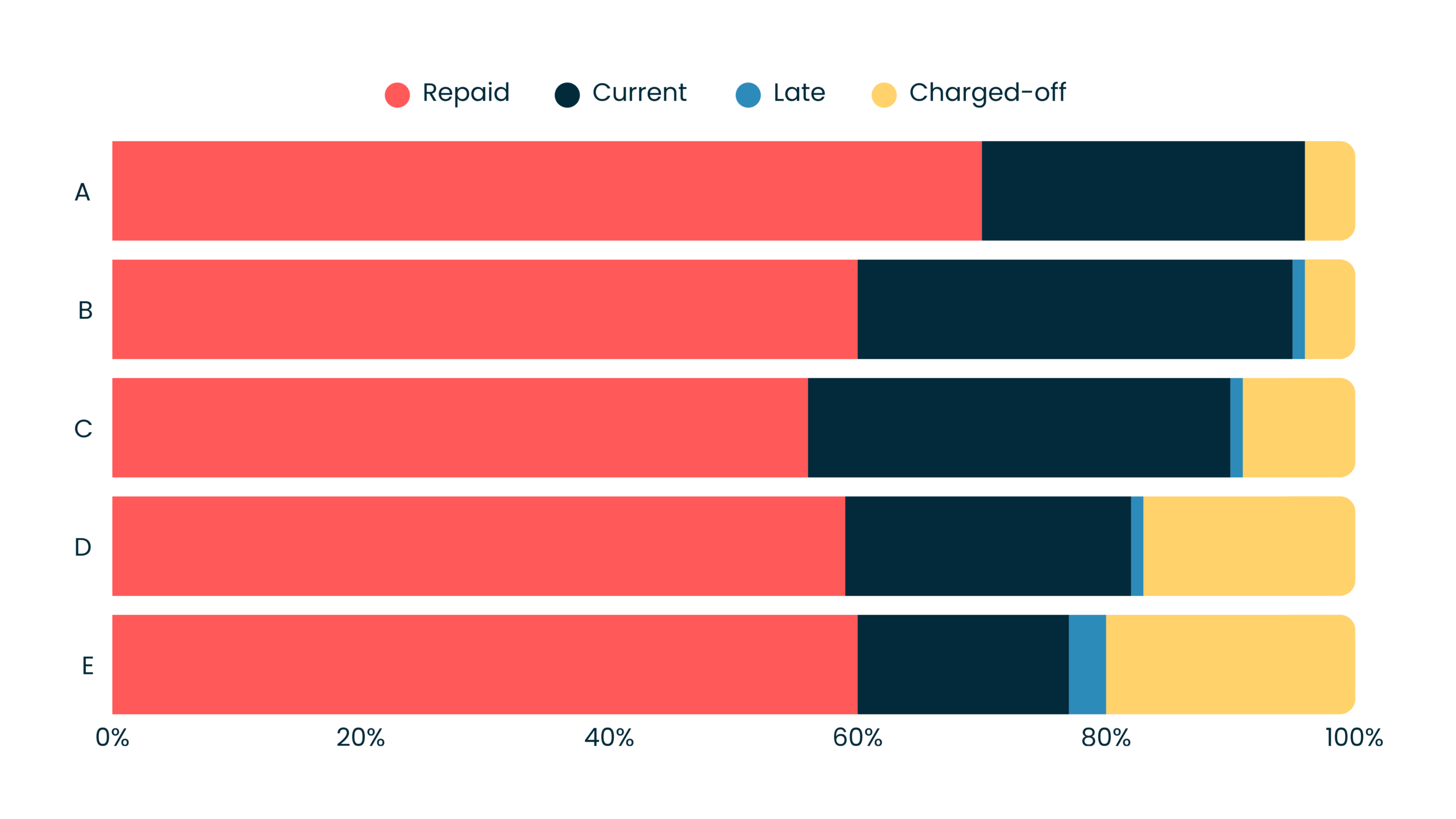

This chart shows the historical status of loans across each loan grade. While repayment outcomes vary by grade, no single grade is entirely risk-free, reinforcing the importance of building a diversified portfolio.

Based on historical goPeer loan performance as of March 31, 2026. Loan status percentages represent the proportion of loans within each grade that are repaid, current, late, or charged off. For reporting purposes, the A grade includes subgrades A+, A, and A-; the B grade includes B+, B, and B-; the C grade includes C+, C, and C-; the D grade includes D+ and D.

The bottom line

No lending platform is absolutely free from any delinquency or defaults. But transparency around how these situations are managed is important.

At goPeer, collections’ efforts begin early, and servicing remains throughout the delinquency process. Many late loans are eventually brought back into good standing or repayment arrangements.

While losses are still a part or lending, understanding how collections and recoveries work can provide better context around portfolio performance and long-term investor outcomes.

Disclaimer:

This article is provided for informational and educational purposes only and does not constitute investment, financial, legal, accounting, or tax advice, nor is it a recommendation or solicitation to purchase any security.

The information presented regarding delinquency, recoveries, charge-offs, diversification, and portfolio performance is based on historical goPeer platform data as of March 31, 2026, unless otherwise indicated. Historical results, recovery experience, delinquency trends, and charge-off rates are not indicative of future performance and may not be repeated.

Investing in Payment Dependent Notes involves risk, including the risk of loss of principal. Borrowers may miss payments, enter insolvency proceedings, default on their obligations, or otherwise fail to repay their loans. Collection, servicing, and recovery efforts may reduce losses in certain circumstances but do not guarantee repayment of principal or interest. Investors may experience partial or total losses on individual investments.

References to diversification are provided for educational purposes only. Diversification does not guarantee positive returns, prevent losses, or protect against market or credit risk.

Any performance information, examples, statistics, or illustrations are provided to help explain how the platform operates and should not be interpreted as a prediction, projection, or guarantee of future results.

Prospective investors should carefully review the applicable Offering Memorandum, risk factors, and related disclosure documents before making an investment decision. Investment decisions should be based on an investor’s individual objectives, financial circumstances, risk tolerance, and suitability assessment.